Is the auto market in the middle of the year as everyone expected at the beginning of the year? China’s passenger cars have entered a zero-sum game? Does the rising inventory pressure really make people feel chilly at the retail end? The trend of miniaturization of engine displacement is the rigidity of the market The demand is still the policy; what are the market opportunities behind the joint ventures between Aisin, Geely and Guangzhou Automobile; the sales targets of the auto companies in the middle of the year are still announced, and several are happy and sad; the new energy market is under the influence of policy-driven changes and is advancing all the way; the market With consumption weakened, what will happen to the market in the second half of the year? The editor compiled the auto market data from January to June 2018, and summarized and forecasted the supply and consumer markets of the domestic passenger car market in the past six months.

The market enters a zero-sum game, and rigid consumer demand weakens

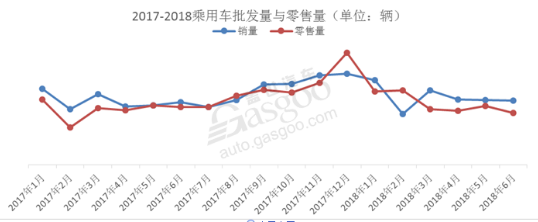

China's passenger car market has experienced rapid growth to the stage of micro-market growth, and independent brands have quickly achieved market sales accumulation and market share increase by virtue of this shareholder style. From January to June 2018, the retail market of the passenger car market continued to shrink, consumer demand continued to weaken, manufacturers and channels inventory pressure continued to increase, and the inventory coefficient reached the highest 1.99 in June. Why does the market both show zero sum The situation of the game, there is a situation of weakening consumer demand, mainly from the following aspects to make a brief analysis.

First, from the perspective of the overall macroeconomic environment, it has brought greater downward pressure on the auto market. In terms of economy, although the GDP growth rate is in a steady growth trend, the growth rates in the first and second quarters were 6.8% and 6.7% respectively, but investment and consumption showed a certain decline, resulting in insufficient consumer confidence and a certain degree of consumption in the auto market. In terms of real estate, since 2018, the activity of real estate transactions in some regions has increased, especially in second- and third-tier cities where the consumer market is growing rapidly, which has caused a decrease in inflows to the auto market, resulting in a delay in auto consumption; in terms of auto consumption, the National VI policies The impact of Sino-US trade frictions and the reduction of import tariffs has increased consumer wait-and-see sentiment.

Second, from the perspective of the development cycle of the auto market, the market has gradually entered a zero-sum game period. The auto market has gradually entered a stage of micro-growth from the stage of rapid development. With the rapid growth of the SUV market, its growth rate has slowed down. The year-on-year growth rate in June was close to zero. The growth rate of sedan is the first time in recent years that the growth rate of SUVs has exceeded that of SUVs. Has gradually receded, and the consumer market has entered a stage of rational consumption. According to the prediction of the Gasgoo Research Institute, the compound growth rate of the SUV market in the next few years will be around 3%. The era of rapid market growth driven by SUVs has passed. The overall market competition has become more intense, and the overall market has entered a zero-sum game period.

Third, from the perspective of consumer demand in the entire market, rigid demand has weakened, and market growth has shifted from incremental to stock. First of all, the market consumption overdraft is obvious. Since the introduction of the purchase tax policy in 2015, the sales of small-displacement vehicles have increased rapidly, but it has also led to the advancement of the car purchase and redemption cycle. Early consumption has led to the weakening of rigid consumer demand in the first half of 2018. Consumers have already purchased cars. No longer urgent. From the perspective of market growth and stock, the number of passenger cars in 2017 has reached 174 million, and the number of passenger cars per 1,000 people has reached 125 vehicles per person. The market development stage has undergone major changes, and the incremental market The stock market has transformed significantly.

Is the trend of miniaturization of engine displacement due to rigid market demand or policy

With the introduction of national energy conservation and emission reduction policies and fuel consumption regulations, and the complete decline of the small-emission purchase tax policy, small-emission vehicles have experienced ups and downs. Does the consumer market favor cars with low-displacement engines, or does policy drive automakers to continuously deploy small-displacement cars? This article will analyze the following aspects.

First, from the point of view of the national energy conservation and emission reduction policy, as the automobile is a major consumer of fuel consumption and carbon emissions, it is imperative to transform and upgrade. From the perspective of the Made in China 2025 development strategy, the 13th Five-Year National Strategic Emerging Industry Plan, and the long-term plan for the automobile industry, it is imperative to save energy and reduce emissions, and the development of small-displacement vehicles is also taking advantage of the trend.

Second, from the perspective of fuel consumption regulations, regulatory requirements are becoming increasingly severe, and engine miniaturization has become a battleground for manufacturers. In 2016, my country officially entered the fourth stage of the most stringent fuel consumption limit in history. It is required that from 2016 to 2020, the average fuel consumption of passenger cars produced by all car companies must be reduced to 5L/100km, and to 4L/ by 2025. One hundred kilometers, car companies are under tremendous pressure, and miniaturization of engine displacement has become an inevitable choice for car companies to respond to fuel consumption regulations. In particular, the blessing of three-cylinder engine models and 48V systems will help automakers respond to fuel consumption regulations.

Third, from the perspective of market demand, engine miniaturization needs to be tested by the market. Since the introduction of the purchase tax, the market share of small-displacement vehicles has risen rapidly, and at the same time, the consumption of some small-displacement vehicles has been overdrafted ahead of schedule. Especially the three-cylinder engine models have been launched on the market. The economy is better and the power parameters have also been effectively improved, such as Focus 1. The 0T three-cylinder engine has a maximum power of 94kW and a maximum torque of 167N/m, both surpassing the maximum power of the 1.6L engine of 92KW and 159N. m maximum torque. At the same time, the new Yinglang, Lynk&Co 02, BMW 1 series and other models have been deployed with three-cylinder engine models. However, its problems also make consumers have doubts, mainly because the three-cylinder engine has poor output continuity and large jitter , Noise, etc. Whether the three-cylinder engine model is to the taste of consumers still needs to wait for the test of market consumers.

In short, engine miniaturization will be the direction of future development. It is not only the national energy saving and emission reduction direction, but also the favorable measures for car companies to respond to fuel consumption regulations. However, products will eventually need to be marketed for consumers to buy. To be recognized by consumers, the market needs to be tested.

Behind the joint venture between Aisin, Geely, and GAC is that there is greater room for development in automatic transmissions in the future

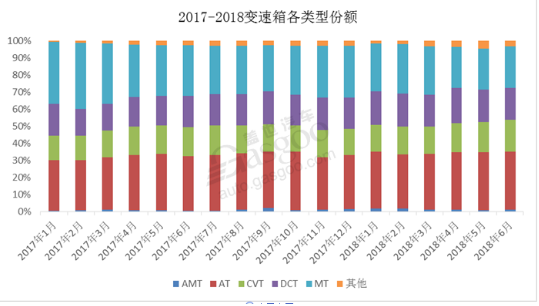

With the rapid growth of sales in the domestic auto market, consumers have higher requirements for vehicle configuration and vehicle control and comfort. Consumption upgrades have also brought changes in various segments of the auto market, and gearboxes are one of them. According to the analysis and analysis of drive system data products, the domestic sales of models with automatic transmissions have risen to 60% in 2017. Among the current automatic transmissions, AT has the highest proportion, and the proportion from January to June 2018 Both reached more than 33%. The joint venture between Aisin, GAC and Geely reflects that there is greater room for the development of automatic transmissions in China in the future, which is mainly analyzed from the following aspects:

First, the gearbox matching situation of domestic production models is mainly independent manual gearboxes, while joint ventures mainly rely on automatic gearboxes. In the entire automobile sales market, the 5MT and 6MT gearboxes of independent brands are mainly used in low-end and medium-end models, while foreign brand models are mainly equipped with automatic transmission models, showing that China is a major consumer of gearboxes. But it is not a strong country in gearbox production. There are relatively large technical barriers in gearbox technology, which has become one of the obstacles to the upward development of independent brands.

Secondly, it has become a demand for market development to be equipped with automatic gearboxes. According to Gasgoo’s share of gearbox types in various models from January to June 2018, the share of automatic transmissions rose from 70% in January to 72% in June. With the development and improvement of transportation infrastructure, consumption upgrades and Consumers’ increased vehicle configuration and performance requirements, whether it is a model with a price drop or a self-developed high-end brand, is the first choice considered by most consumers.

Third, the improvement of the quality of core components equipped with models is an inevitable choice for the high-end of independent brands. Driven by the SUV dividend, the product quality of independent brand car companies has begun to approach the level of joint venture brands. The prices of self-owned brand models have risen to grab the mid-to-high-end joint venture brand market. It is an inevitable trend to be equipped with automatic transmissions. Geely Lynk & Co 01, Great Wall WEY VV7, Roewe RX5 and other models are equipped with 7-speed DCT gearboxes, while all Trumpchi GS8 series are equipped with 6-speed AT gearboxes. In the future, in the market share of independent brands, the sales share of automatic transmission models will rise rapidly, and even the sales of automatic transmission models will occupy the main share like joint venture brands.

Reshaping the competitive landscape of auto companies, Geely and SAIC take the lead in the growth of independent brands

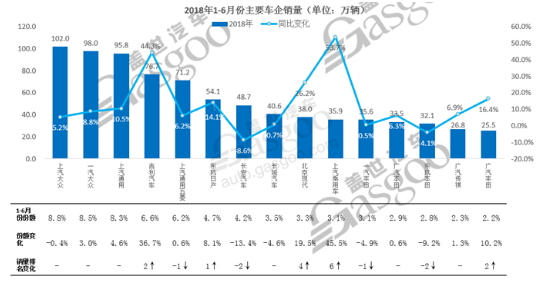

In the first half of 2018, the sales volume of the passenger car market was sluggish, competition among auto companies was fierce, and the competitive landscape showed new changes. The strong were stronger, mainly in the following aspects:

First, the German department is still on the list. The joint venture brands North and South Volkswagen and SAIC GM have benefited from the new product cycle, and the top three sales have remained unchanged, while FAW-Volkswagen and SAIC-GM both have growth rates higher than the average growth rate of the automobile market by 5.6%, and their sales share has increased steadily;

Second, the sales of independent car companies are blooming. Self-owned brand car companies, Geely and SAIC Passenger Vehicle, continue to make breakthroughs with their respective product strengths, and their market performance is remarkable, becoming the leading companies of self-owned brands; Geely's ranking has risen by 2 places, with a year-on-year increase of 36.7%, and its entire series Product sales are relatively balanced, with SUVs and cars achieving balanced development. SAIC's passenger car sales ranks up 6 places, with a year-on-year increase of 45.5%, mainly due to the better sales of Roewe series models. Affected by the slowdown in the growth rate of SUV sales, Great Wall and Changan Automobile both showed different degrees of decline. In particular, the decline of Changan Automobile was relatively large, mainly due to the relatively large decline in sales of CS series models;

Third, the sales growth of Japanese auto companies was mixed. Among Japanese brand car companies, sales of Dongfeng Nissan and GAC Toyota have increased, while sales of other Japanese car companies have stagnated or declined. In particular, Dongfeng Honda's sales fell by nearly 9% due to the engine oil incident, and its sales ranking fell 2 places.

It can be seen from the competition pattern of various enterprises that in the increasingly competitive passenger car market, consumers are more rational in consumption, and the product requirements must have both external appearance and internal quality, and the competition of product strength has become the competition of various enterprises. An important weight in the game between.

Policy-driven new energy passenger vehicles "quantity" and "quality" continue to hit new highs

In the first half of 2018, the new energy passenger vehicle market continued to grow strongly, with a total sales of 268,800 vehicles, a year-on-year increase of 210%, accounting for 2.8% of the overall passenger vehicle sales. The new energy passenger vehicle market is mainly driven by policies. From January to June 2018, it started well, and its volume and quality reached new highs, which are mainly manifested in the following aspects:

First, from the perspective of policy performance, the policy-driven effect is obvious. The period from February 13th to June 12th was the transitional period of subsidies, which prompted consumers to consume in advance in June, leading to rapid growth in sales and growth in January and June, and the implementation of the new subsidy policy resulted in a significant decline in sales in June. , The market sales are more obviously affected by the subsidy policy.

Second, from the overall fuel type, pure electric leads the market sales growth, and the plug-in hybrid base is small and fast. The sales of pure electric vehicles in the first half of the year totaled 189 thousand, mainly concentrated in A00-class vehicles. The main sellers are BAIC New Energy, Jiangling New Energy, Zhidou and other brand models, and second-tier and lower-tier cities have become its new sales growth. source. The base number of plug-in hybrids has a small growth rate, and the growth rate is higher than that of pure electric sales. The sales volume totals 79,000, mainly concentrated in A-level models. Roewe and BYD are the main best-selling models in this field, and their consumer markets are mainly In first-tier cities such as Shanghai, Guangzhou and Shenzhen, its product strength has gradually been recognized by consumers.

Third, from the perspective of manufacturers' product layout, the policy is forcing manufacturers to transform and upgrade their product structure. From January to May, the product structure of the market is dominated by A00-class models. During the period of the new subsidy policy, the share of A00-class models has dropped significantly, while the share of plug-in hybrid cars has risen to 30%. Manufacturers can get more subsidies to satisfy consumers. In line with the demand for cruising range, automakers will follow policy changes to launch more models with better product power, longer cruising range, higher battery energy density, and lower power consumption.

Fourth, from the perspective of regional factors, sales in different regions are quite different. On the one hand, the current new energy subsidies are mainly divided into national subsidies and local subsidies in some regions, resulting in large differences in the price of new energy in various regions, and the inability to achieve a national uniform price, which is one of the obstacles hindering the promotion of new energy vehicles; second; On the one hand, the consumption situation in different levels of cities is inconsistent. The sales base of new energy in cities with restricted purchases is large but the growth rate is slowing, while the market in cities with non-restricted purchases is broad. Consumers mainly prefer A00-class vehicles with better cost performance; third, sales of models in various regions Affected by manufacturers and local factors, Shandong, Henan, Changsha, and Guizhou are mainly low-speed electric vehicle sales provinces, while sales in cities such as Guangzhou, Shenzhen, Shanghai, Nanchang, and Liuzhou are more affected by the location of manufacturers.

Passenger car market outlook in the second half of the yearUnder various factors such as the economy, real estate, and market cyclicality, the sales of passenger vehicles in the first half of the year increased by 5.1% year-on-year. In the second half of the year, the downward pressure on the economy was greater, the real estate regulation continued to tighten, and the market was cyclical Other factors still exist, and the uncertainty of Sino-US trade will continue to affect the sales market. With the implementation of the tariff policy, the wait-and-see sentiment has weakened. At the same time, sales in the second half of the year are the peak season for auto market sales. It is believed that the auto market will continue to maintain low growth in the second half of the year.

In terms of the overall passenger car market, under the pressure of high inventory in the first half of the year, passive production, destocking and price reduction promotions will become key tasks; the third to fourth quarters have always been the peak season for market demand, and the consumer demand of the wait-and-see and unconsumed consumer groups in the first half of the year will be There will be some release, and the gradual improvement of the auto market will be certain; the market stock base will become larger, and the incremental growth pressure will be greater, and the overall stock conversion growth momentum will gradually be released;

In terms of powertrain, more new cars will be equipped with small-displacement engines in the second half of the year, and automatic transmissions will be carried by more self-owned brand models, mainly in AT, DCT, CVT and other types;

In terms of the pattern of passenger car companies, the North and South Volkswagen has launched more products, and the sales momentum will be fully released in the second half of the year; the self-owned brand Geely and SAIC passenger car product portfolios continue to strengthen, sales continue to rise, and the entire self-owned brand will appear stronger , The weaker have more pressure;

In terms of new energy passenger vehicles, policy-driven sales will maintain rapid growth. The share of A00-class models will continue to be the main market force, plug-in hybrid models will grow steadily, and the overall structure will undergo significant changes due to the growth of new subsidies. At the same time, they will be launched in the second half of the year. Most of the new cars will be A0 and above models, mainly to meet the new subsidy policy, on the one hand to get more subsidies, on the other hand, to enhance product capabilities to meet consumer needs;

Considering the economy, policies, and the auto market's own factors, analysts at the Gasgoo Research Institute believe that the market growth rate in the second half of 2018 will be lower on the basis of the high base in 2017. For the whole year, the market growth rate will remain at about 3% compared with the same period last year. Competition in the zero-sum game period in the market tends to intensify, the growth of the auto market shifts from incremental to stock, and consumer demand is more inclined to rational and practical consumption. The overall auto market "volume" changes slow down, and the "quality" changes tend to be "predictable." .

Car Antenna for Wifi,Car Radio Antenna,Car GPS antenna,FM AM Car antenna

Yetnorson Antenna Co., Ltd. , https://www.xhlantenna.com